Wen | Xiao Gu Dong

In the first 25 minutes, the heat value broke 21,000, and the heat value broke 22,000 the next day. Tencent’s video love social reasoning reality show "Heartbeat Signal 7" entered the Love Watch Club on the day of the first program launch, and entered the Must Watch Club the next day.

The rising heat value is a true portrayal of the "seven years without itching" achieved by the content of continuous innovation in "Heart Signal 7". However, when we cast our eyes on the level of investment promotion, the opening broadcast of the first program of Heartbeat Signal 7 only contained the exclusive title Oreo and the industry sponsorship Taobao, which seemed to indicate that even in the "comprehensive N generation" with steady and innovative content, the related investment promotion bonus was disappearing, and the attraction at the TO B level began to decline, and it was urgent to develop new growth points.

Before the "Heartbeat Signal 7" was launched, there were media statistics that there was no general title for the love healers launched this year, and nearly half of them were streaking. As the "originator of love", the launch of "Heartbeat Signal 7" has broken this situation to some extent, but it is also an objective fact that the number of cooperative brands has been greatly reduced compared with before.

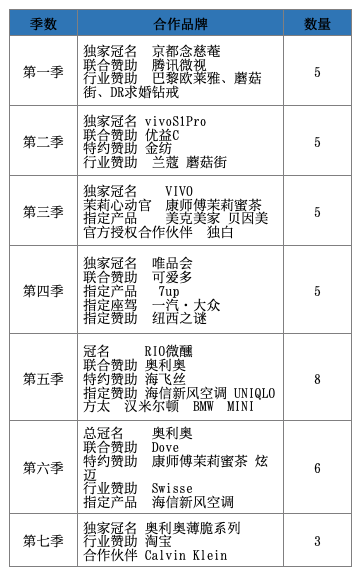

In this regard, Reading Entertainment Jun counted the general situation of the cooperative brands of the first phase of the seven-season program "Heartbeat Signal":

Judging from the types of co-brands, "Heartbeat Signal" mainly attracts fast-moving consumer goods such as personal care, fabric cleaning, food and beverage, drinks, and several major types such as automobiles, mobile phones, electrical appliances, shopping apps, short videos, etc. In the seventh season, the co-brand types are only fast-moving consumer goods and shopping platforms.

Judging from the continuity of brand cooperation, VIVO, Master Kong Honey Tea, Hisense Xinfeng Air Conditioning, Oreo and Mushroom Street have all cooperated twice, while the other brands have cooperated once.

Judging from the number of cooperative brands, there were five cooperative brands in the first four seasons, eight reached the peak of cooperation in the fifth quarter, and only three in the seventh quarter.

Today’s situation is not only closely related to the recession of the variety industry, but also related to the limitations of the IP of Heartbeat Signal at the audience level.

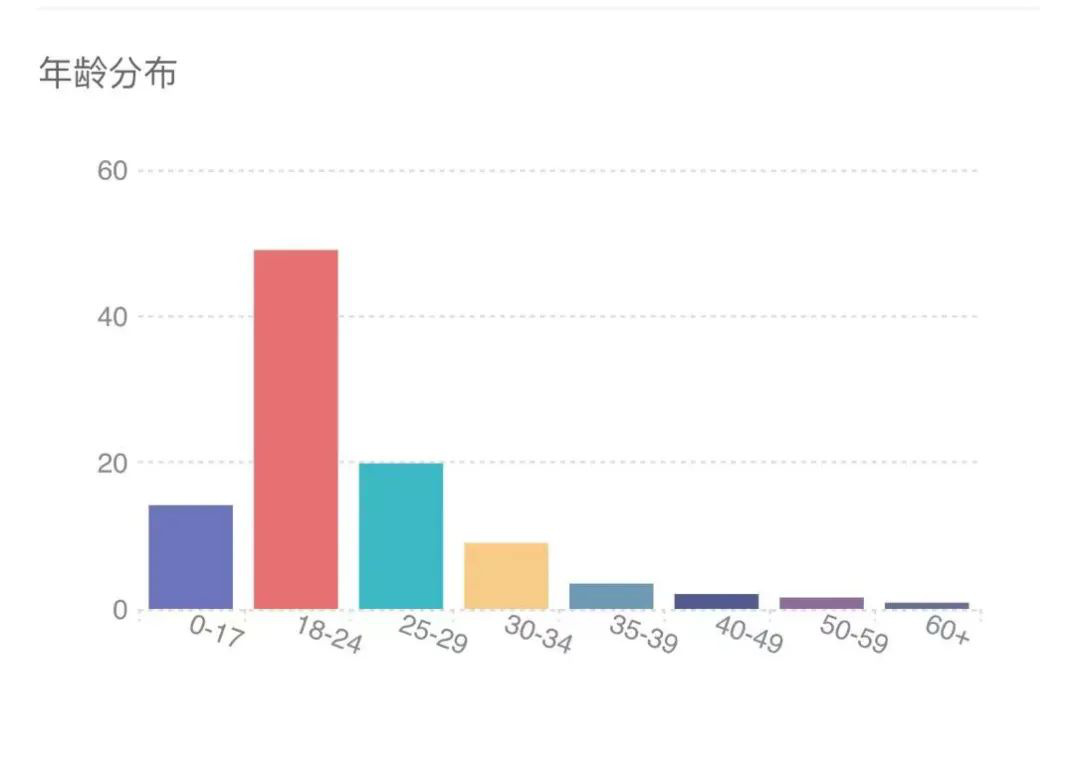

The number of entertainment shows that the proportion of users under the age of 24 in Signal of Heartbeat is over 60%, and most of this group are students. Objectively speaking, this group has a strong desire for consumption, but most of them have limited consumption power because they are not completely economically independent, so fast-moving consumer goods with large demand, relatively low price and short life cycle are more attractive and purchasing power to them, while "big products" such as air conditioners and automobiles are not just needed.

Coupled with the changes in the environment of the variety industry and the impact of other content products, "Heartbeat Signal 7" has gradually lost its appeal to many categories of brands, so the categories and quantities of cooperation have become less and less. After all, brand launch not only pursues exposure, but also needs real conversion rate. In other words, the traditional business model of To B has been an economic constraint for the development of love variety, and it is urgent to expand the realization channel to To C, so "Heartbeat Signal 7" has taken a step forward in the innovation of increasing income.

In recent years, the platform and producers have been exploring the mode that the love variety does not rely on advertising revenue to survive. For example, in the first season of "Half-cooked Lovers", the cost was covered by membership income under the condition of attracting investment, which is a typical example. However, at the moment when the number of love stories has dropped sharply, there is no title or even naked broadcasts are normalized, Signal of Heartbeat 7 chooses the way of "diversification" to break the game.

In the seventh season, Heartbeat Signal has accumulated a certain amount of loyal audience, attracting more users to become paying members by drawing surrounding gift packages and winning signature photos. At the same time, "Heartbeat Signal 7" is still exploring more ways for paying members to play-on the basis of VIP watching in advance, SVIP is introduced to watch the feature film 17 hours in advance, watch the reality show 7 hours in advance and the derivative content "Watching Heartbeat with You".

Taking this as a "bait", "Heartbeat Signal 7" raises the threshold for watching ahead of time with higher fees, so that the user groups of earlier dramas can earn money for it, and finally expand new growth points on the basic disk of the original members and expand the space for realizing the program.

According to Reading Entertainment Jun’s observation, most of the variety shows of Tencent Video now serve SVIP in the form of derivative programs to watch in advance. For example, the surrounding contents such as gratifying advance business, chat derivative and punishment derivative of Wonderful Night, and the derivative program "Friends and TA’s TAlk Show" of "Friends and Ta’s Friends" are for SVIP to watch first. That is to say, although SVIP watched an episode in advance for a long time in the drama section, SVIP watched the variety feature film in advance or was the first to eat crabs in Heartbeat Signal.

As early as when it was broadcast in Joy of Life, watching an episode of SVIP in advance caused a lot of controversy. Some netizens said that launching SVIP on the basis of VIP was a doll-making behavior, which caused a lot of discussion on the Internet. Compared with watching an episode in advance, SVIP has more priority rights and interests in Heartbeat Signal and its derivative content, and it also causes more disputes.

This is due to the suspense nature of Heartbeat Signal 7 itself, and the play of SVIP feature film in advance has further advanced related marketing and discussion, which has forced users who have not watched the program to accept "spoilers" on social platforms, greatly weakening their expectations and interest in related content.

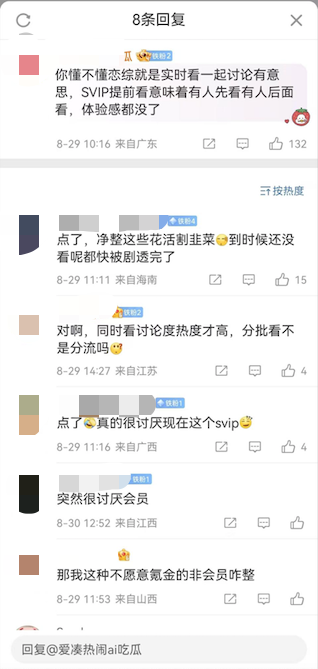

In this regard, some netizens commented in Weibo, the official website of Heartbeat Signal: "Do you understand that it is interesting to watch and discuss together in real time, and SVIP watching in advance means that some people watch first and others watch later, and the sense of experience is gone." In this regard, many netizens agreed: "Clean up these flowers and cut leeks alive, but I haven’t seen them yet, and they will soon be spoiled" …

During the broadcast of the program, SVIP can watch derivative content and feature films in advance, which is undoubtedly another expansion of content rights. For VIP, this is the shrinkage of related rights and interests, and it has greatly affected the user’s viewing experience. In addition, "Heartbeat Signal 7" allows SVIP, VIP and ordinary users to watch the program in three batches, which diverts the real-time popularity of the program to a certain extent, and even intensifies the spread of program content outside the platform in the form of network disk links. The rampant pirated content may make the program group lose more than it gains.

Experienced platform parties and program groups can certainly predict these problems arising from the expansion of SVIP rights and interests of Heartbeat Signal 7. However, at the moment when it is difficult to attract investment, Heartbeat Signal 7 still chooses to explore more ways of realizing it at the expense of user experience, diversion of program popularity and rampant piracy. This is like "drinking poison to quench thirst" and "really hating this SVIP now".

Selling peripheral products is another way to realize heartbeat signal 7. Judging from the products on the shelves in the special area, most of the peripheral products are life products designed in the name of heartbeat, mainly including straw cups, pillows, Rubik’s cube bracelets and necklaces, placemats and aromatherapy pendants.

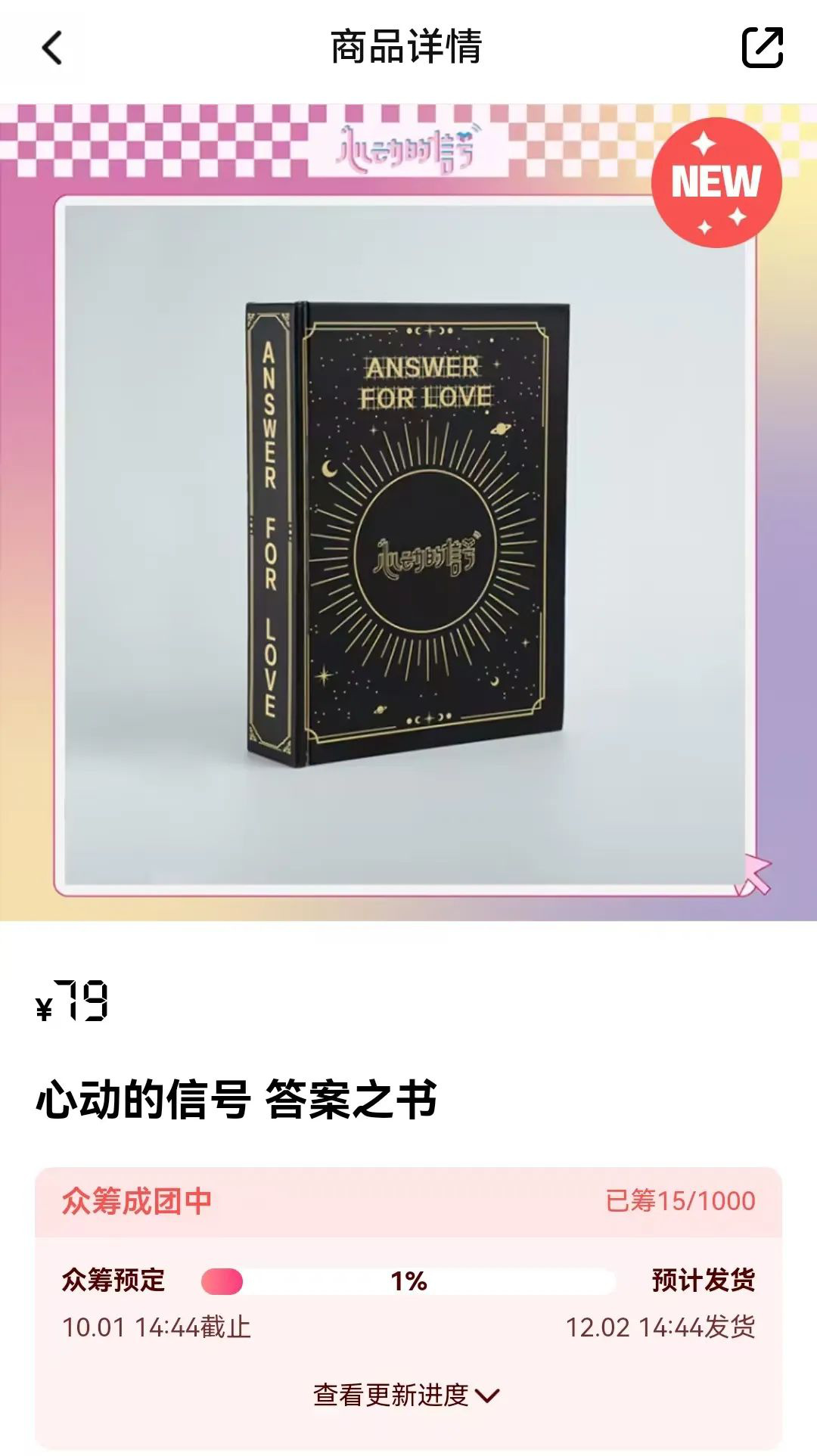

Reading Entertainment Jun noticed that the top three bestsellers were 59 yuan’s straw cup, 79 yuan’s answer book and 12.8 yuan key chain. Among them, the answer book was sold in the form of crowdfunding, with a target of 1,000 copies, but only 15 copies were raised by crowdfunding before the draft, and this sales volume corresponds to the third place, which seems to indicate that the sales of peripheral products of Heartbeat Signal 7 are not ideal.

In addition, "Heartbeat Signal 7" also opened the game of cloud booking for fans (cloud booking is a product launched by Tencent Video at the end of 2023 and used in popular dramas and variety shows on the platform). From the price point of view, the price of "Heartbeat Signal 7" is 50 copies, and 10 copies are available for purchase. The price is higher than that of 30 copies of "Wonderful Night", "Talk Show and Friends of TA", which is higher than that of other programs. Is it value for money or inflated?

On the whole, in addition to the traditional advertising revenue, "Heartbeat Signal 7" expanded its revenue channels by expanding the rights and interests of SVIP, switching VIP and SVIP by lottery, increasing the unit price of cloud booking, and selling peripheral products. This also means that the majority of users will become the core fulcrum of the expansion of love integration from TO B to to TO C represented by "heartbeat signal 7".

With more and more paid names, are users leeks, suckers or others? We don’t know, but it can be predicted that in the future, the psychological cost for users to watch love games will be higher and higher. Perhaps, this is the "price" of the heart!

* Original article, please indicate the source when reprinting.